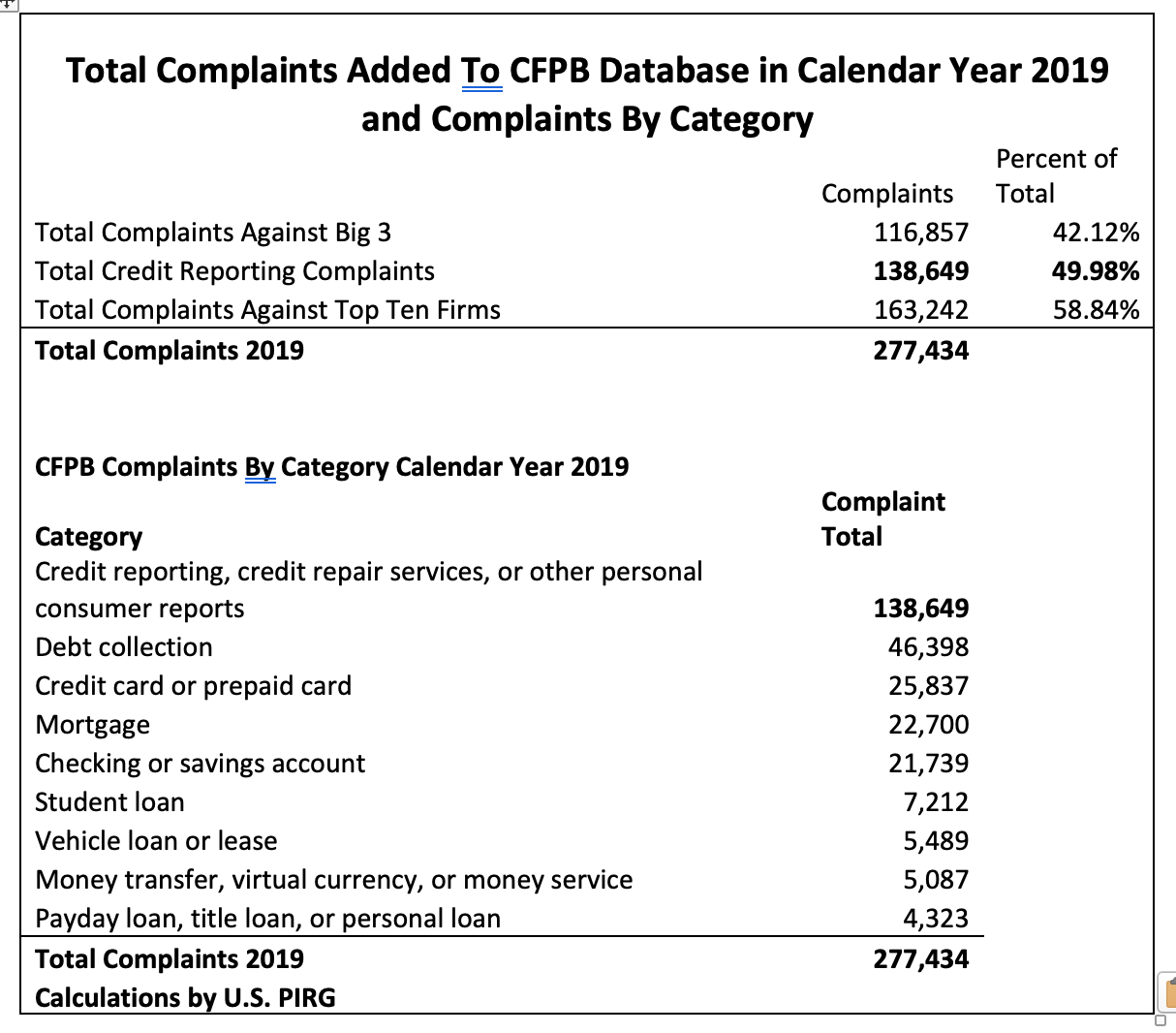

On Wednesday, the full U.S. House is expected to vote on a credit reporting reform package, HR 3621, the Comprehensive CREDIT Act. Meanwhile, a PIRG analysis finds that half of all complaints to the CFPB in 2019 concerned credit reporting and the most-complained about companies, in the entire database, were the so-called Big 3 credit bureaus.

On Wednesday, 29 January, the full U.S. House is expected to vote on a broad credit reporting reform package, HR3621, the Comprehensive CREDIT Act. Meanwhile, a PIRG analysis finds that half of all complaints reported into the CFPB’s Public Consumer Complaint Database in 2019 concerned credit reporting. Further, complaints about the Big 3 credit bureaus led complaints from all other companies, with Equifax (#1), TransUnion (#2) and Experian (#3) leading the “Top Ten” most-complained-about firms.

The Comprehensive CREDIT (Credit Reporting Enhancement, Disclosure, Innovation, and Transparency) Act of 2020 is supported by over 85 leading consumer and civil rights groups, including Americans for Financial Reform, the National Consumer Law Center (NCLC) and U.S. PIRG. Both NCLC and U.S. PIRG testified in favor of the bill at a hearing before the House Financial Services Committee last year. They and other consumer and civil rights advocates described the numerous problems with the credit reporting system, including the extreme difficulty consumers face when seeking reinvestigations of mistakes. Mistakes lower credit scores and cause consumers to pay more, or be denied credit or insurance or even a job.

Key elements of HR3621 would do the following (Note that the House Financial Services Committee had passed six bills on credit reporting, including (HR3621, originally the Student Borrower Credit Improvement Act). For the purposes of floor action, all 6 bills were re-packaged together as HR3621, the Comprehensive CREDIT Act:

This is just a partial list of improvements to the credit reporting system that HR3621, the Comprehensive CREDIT Act, would make to help consumers get a better shot at obtaining credit, insurance or employment. It would also help free consumers from the Kafka-esque nightmare of fixing mistakes on their reports by holding the credit bureaus much more accountable to consumers. We’re not their customers, but they sell information about us. We can’t vote with our feet for a new credit bureau but we deserve the right to make sure that what they say about us is true.

,

Photo credit: danielfela via Shutterstock

Senior Director, Federal Consumer Program, PIRG

Ed oversees U.S. PIRG’s federal consumer program, helping to lead national efforts to improve consumer credit reporting laws, identity theft protections, product safety regulations and more. Ed is co-founder and continuing leader of the coalition, Americans For Financial Reform, which fought for the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, including as its centerpiece the Consumer Financial Protection Bureau. He was awarded the Consumer Federation of America's Esther Peterson Consumer Service Award in 2006, Privacy International's Brandeis Award in 2003, and numerous annual "Top Lobbyist" awards from The Hill and other outlets. Ed lives in Virginia, and on weekends he enjoys biking with friends on the many local bicycle trails.